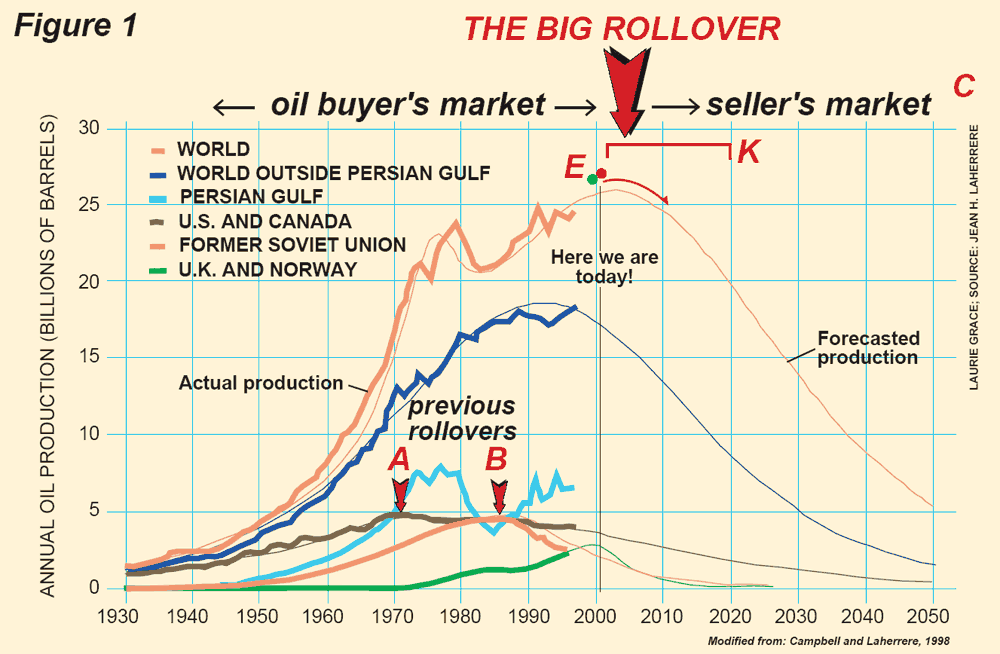

Peak Oil, the Resource Curse and the Green Paradox

Submitted by Wespac Advisors, LLC on February 7th, 2016- A decade ago, the notion of Peak Oil had become everyday reading – Peak Oil, or Hubbert’s theory, was the point in time when the maximum rate of extraction of petroleum is reached after which it is expected to enter terminal decline. Most of the older forecasts called for peak oil to occur somewhere in the 2000-2010 time-frame, forever creating a seller’s market (and higher prices) for crude oil.

- We have now experienced two massive sell-downs in oil in less than 10 years and we are now trading at levels significantly lower than during the 2008 Crisis; is Hubbert’s theory just on hold, or is something else happening here?

- A quick review of the EIA’s Annual Energy Outlook 2015 sheds some light on the underlying fundamentals:

- From 2013-2040, the EIA forecasts annual total production of all US energy types (crude oil, natural gas, coal, nuclear, hydro, biomas and other renewables) to rise 0.9% annually while total consumption of all energy types is forecast to rise just 0.3%; total supply over the next 18 years is expected to outpace consumption for all energy sources in the US.

- From 2013-2040, the EIA forecasts annual total production of crude oil to rise 0.9% while total consumption of petroleum and other liquids (crude oil, ethanol, and biodiesel) is forecast to rise 0.0%; the EIA is forecasting ZERO growth in US demand for petroleum and other liquids for the next 18 years.

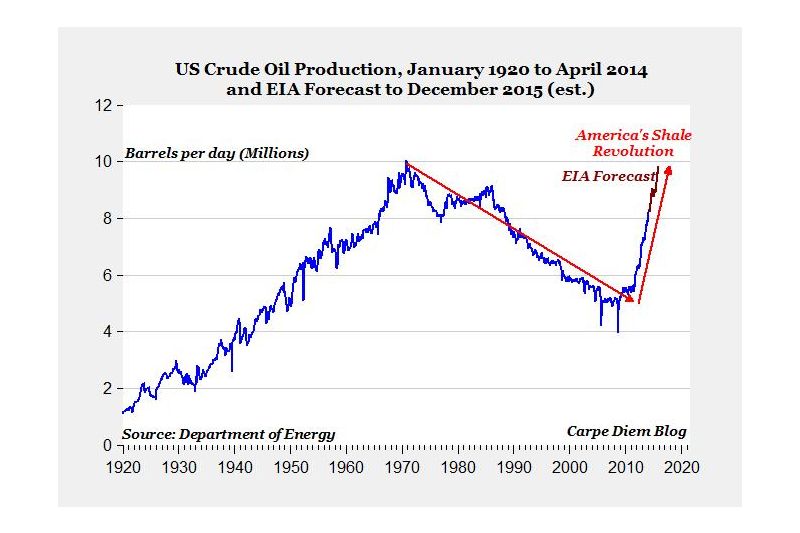

- So, yes, something else is happening here, both on the supply side and the demand side in the US. Here is a nice summary of the supply side disconnect:

- In the absence of the Hubbert effect, i.e. no peak oil in the near term, aren’t low oil prices “unambiguously good for the economy”?

- Harold James at Princeton does not think so:

- “Rapidly changing commodity prices can upend the geopolitical landscape as well, sparking political instability — or worse. And, today, oil seems to be going the way of timber and steel, losing its strategic importance….this is likely to have epochal consequences, as weakening oil prices undermine the authoritarian regimes that control the main producers. There is a large amount of scholarly evidence linking dependence on natural resources with poor governance — “the Resource Curse”. Whatever the many differences among Nigeria, Venezuela, Saudi Arabia, Russian, Iran, and Iraq, all have one thing in common: oil revenues have corrupted the political system, turning it into a deadly struggle for the spoils. As prices fall, the bandits in charge will quarrel more among themselves – and with their neighbors.”

- “The security challenges implied by dropping oil prices are likely to be more significant than the economic risks. But security challenges can be costly.”

- Hans-Werner Sinn at University of Munich, in his book The Green Paradox, points out other unintended consequences. The owners of carbon resources, according to Sinn, are pre-empting future regulation by accelerating the production of fossil fuels while they can. This is the “Green Paradox”, i.e. expected future reduction in carbon consumption has the effect of accelerating climate change. Interestingly, Sinn’s solution to the Green Paradox is to create a “Super-Kyoto” system for a worldwide coordinated cap-and-trade system supported by taxes on capital income to effectively control crude oil supply. Hardly an outcome that Hubbert expected with his Peak Oil theory.

- Foremost in investor’s minds are two important questions:

- Is this collapse in oil prices going to end with a V-bottom as it did in 2009 providing huge investment opportunities?

- Does the collapse in oil prices suggest, as James suggests, a “warning of approaching geopolitical storms”?

- To the first question, the EIA clearly believes the collapse in oil prices is temporary. In their Annual Energy Outlook 2015, they forecast that 2015 will turn out to be a trough in prices and that nominal prices will increase to an average of $75/barrel in 2016 and will resume an uninterrupted rise to $229/barrel by 2040. This is probably the consensus view.

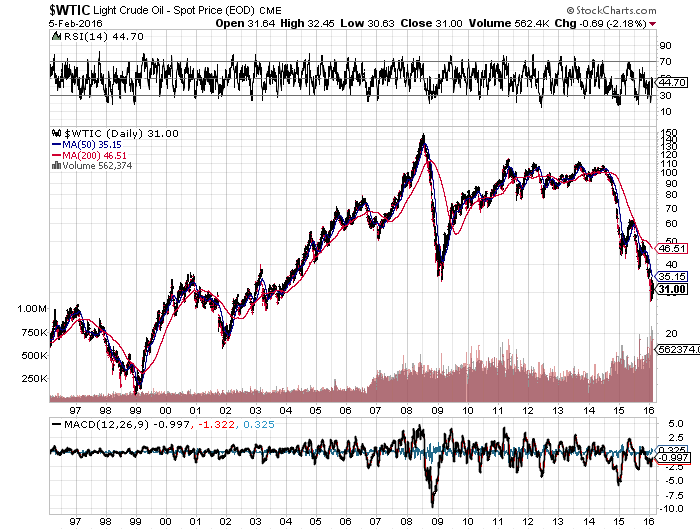

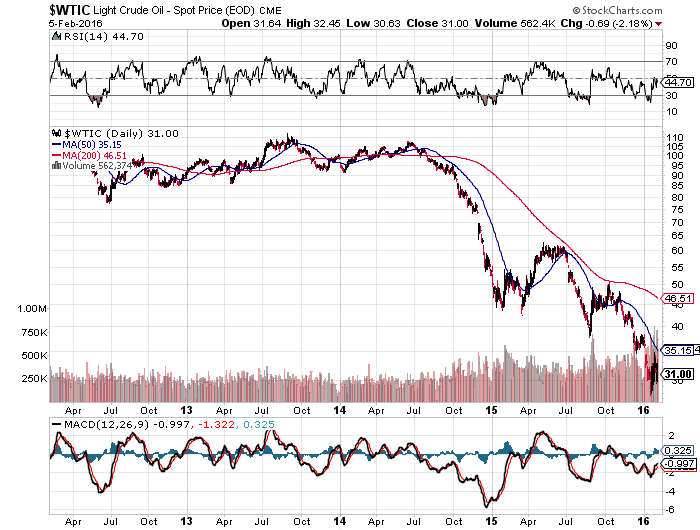

- From a technical point of view, Light Sweet Crude has not traded above its 200-day moving average since mid-2014, which is now in the $46 range. Both the May15 and Oct15 rallies from spike lows were sold heavily once reaching the 200-day. While clearly imperfect, a move above the 200-day would be a first sign of a potential market reversal.

- To the second question, some analysts are suggesting that if oil does not return to break-even levels, estimated to be in the $60 range, over the next 12 months, that there will be significant geopolitical storms brewing as the economies of the main oil producers begin to have very serious financial problems.

- Only one thing is certain in this epic volatility of a commodity so central to the global economy — it is going to cause continued uncertainty and volatility in the equity markets, and, should the EIA be incorrect, i.e. that crude oil prices are “lower for longer”, then this situation has the potential of becoming a major fundamental and psychological catalyst over the coming year.