Market Review & Outlook: October 2018

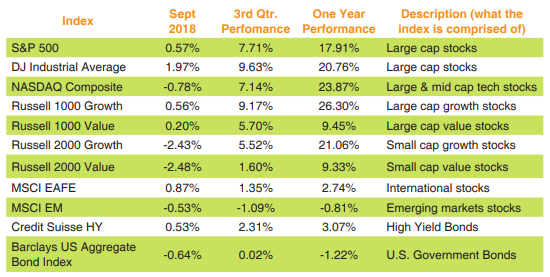

Submitted by Wespac Advisors, LLC on October 16th, 2018We just wrapped up the best quarter for US stocks since the fourth quarter of 2013, with the headline indices all delivering strong performance, despite a variety of challenges. The rate environment continued to challenge fixed income investors, as the bond market was flat for the quarter. Continued strength in the US economy and impressive growth in corporate America were key drivers of stock market performance last quarter. For a closer look at how various stock and bond asset classes performed in recent periods, please refer to the table.

The stock market’s third quarter performance was impressive given the tariff and trade tensions, but those were not the only challenges. Fiscal stresses in Turkey sparked fears of contagion in emerging markets, which entered a bear market in August. The Federal Reserve raised interest rates for the eighth time this cycle last week and is on track to hike again in December. Long-term interest rates rose during the quarter, but the yield curve stayed flat in what some believe may be a sign of coming economic weakness. The upcoming midterm elections introduce policy risk. Add to all that the fact that the third quarter has historically been the worst quarter for the stock market and stocks sailed right through all of these headwinds, extending the longest bull market ever (depending on how one measures such things).

The US economy grew at a very robust 4.2% annualized rate during the second quarter, which is probably not sustainable. However, with continued support from fiscal stimulus, consensus expectations are that growth will come in at 3% for the third quarter, based on Bloomberg forecasts. Business confidence is strong, and small business confidence reached its highest level since 1973 in August, according to the National Federation of Independent Business. Consumers remain upbeat as well, with the Conference Board’s consumer confidence measure at an 18-year high. Job growth remains steady and incomes are accelerating, though not enough to worry the Fed.

In addition to the strong performance of the US economy, corporate America delivered one of its best quarters of earnings growth in decades, supported by the tax reform that passed in late 2017. The third quarter is likely to bring more stellar earnings growth – probably over 20% based on Thomson Reuters’ consensus estimates, and this would be the third consecutive quarter or earnings growth over 20%. Overall, the vast majority of the recent data reflect a solid backdrop for the economy, but it’s not all good news. The housing and auto markets cooled some, tariffs have started to curb some capital investment, and economic momentum in Germany, Italy, and the Eurozone generally is very negative.

While the strength in the US economy continues to offer long-term support to the equity markets, the technical backdrop is less compelling. The healthiest markets exist when the uptrend is broad-based, which is not where we find ourselves presently. Over the past several weeks as the headline averages have moved higher and hit new all-time highs, there have been as many stocks on the New York Stock Exchange (NYSE) hitting new 52-week lows as new 52-week highs. In fact, on October 2, The Dow Jones Industrial Average closed at another new all-time high, yet there were 3 times as many 52-week lows as 52- week highs on the NYSE. Since 1965, that has happened on exactly one other day, which was on December 28, 1999 – about two and half months before the 2000-2002 bear market started.

Furthermore, 40% of stocks in the S&P 500 are down on the year, with fewer and fewer stocks responsible for the gains as the year has moved along. Nearly all of the gains for the year have been concentrated in just three sectors: technology, health care, and consumer discretionary. In addition, while the NASDAQ sits near a record high, only 49% of stocks in the index trade above their 200-day moving average. These divergent trends also extend to the domestic small cap and overseas markets. Although the US is the only important equity market sitting at new highs, small stocks as measured by the Russell 2000 underperformed the large cap indices during the quarter and weakened significantly in September. Strangely, defensive stocks have been leading the market lately (since 6/1), something that has historically spelled trouble ahead for the economy and markets. According to Jim Paulsen, chief investment strategist of The Leuthold Group, “for a stock market supposedly driven by some of the best economic performance of the recovery, its leadership seems out of whack.” Looking at data from 1948 to 2018, Paulsen found that defensive stocks began to show strong relative performance prior to every recession in the US during that time.

Finally, on a historical basis, bull markets are generally a global phenomenon with major moves enjoyed by the vast majority of worldwide stock indices. Although the US market could continue to rise in isolation, the most powerful historical rallies have taken place when the move is global in nature. Many pundits anticipate a year-end rally developing after the November elections. The fourth quarter has been the most seasonally strong for stocks for decades and that especially applies to years where there have been mid-term elections. Indeed, the fourth quarter of midterm years kicks off the best three-quarter span of the four-year election cycle. Combined with the first and second quarters of the third year of a presidential term, that nine-month stretch has averaged a 20.4% gain for the Dow and a 21.1% rise for the S&P 500 since 1949. Moreover, a recovery in world stock markets beginning in the fourth quarter would strengthen the argument that stocks are poised for a significant move higher that carries well into 2019. With the US closing the trade deal with Canada and Mexico last week and continuing to work on the China deal, continued success in this area could help spark a recovery overseas.

As we have stressed in past writings, investors should not be complacent, as valuations in US stocks continue to rival those of the most overvalued markets in history, including 1929 before the Great Crash and 1999-2000 prior to the bear market of 2000- 2002. There was just an article in the Wall Street Journal on October 1 pointing out that the current market is the most forgiving of IPO’s that have no earnings of any time period since the 1999-2000 era when all the internet start-ups went public (and then many went bankrupt). The fixed income market continues to be challenging for investors. While we anticipate that rates will continue to rise modestly and provide a headwind for bonds, we certainly believe that suitable investors should continue to hold bonds to provide cushion in the event of market declines. As always, it never hurts to take stock of your overall positioning in your retirement portfolio to make sure your risk/return profile is the most suitable for your personal facts and circumstances.

If you have a general administrative question about your account, please contact our customer service at 800-535-4253 option 1. If you need investment advice, please contact your firm’s designated consultant or me. You can reach me at extension 1178 (510-740-4178) or at john.w@wespac.net. John Williams, Manager of Advisory Services – WESPAC