Market Review & Outlook: April 2018

Submitted by Wespac Advisors, LLC on October 16th, 2018Volatility is back. After one of the least volatile years in stock market history, 2018 is shaping up to be more normal from a volatility perspective – or perhaps even more volatile than normal. Stocks sprinted out of the gate in the US to start the year, as the headline averages gained more than 6% during January and continued the impressive run of performance that had been in place since the presidential election in November 2016. Since Trump won the general election, stocks soared on the hopes – and eventual implementation – of a number of business-friendly initiatives, that both Corporate America and Wall Street welcomed. The investment community has been most emboldened by the drastic cutback in financial regulations and the passage of the most comprehensive tax-reform plan in decades, the latter of which cut the corporate tax rate from 35% to 21% and lowered taxes for more than 80% of Americans. President Trump’s business friendly policies, along with a strengthening U.S. economy, a still-accommodative Federal Reserve, and strong earnings results from the corporate world, appeared to be the perfect cocktail for investors.

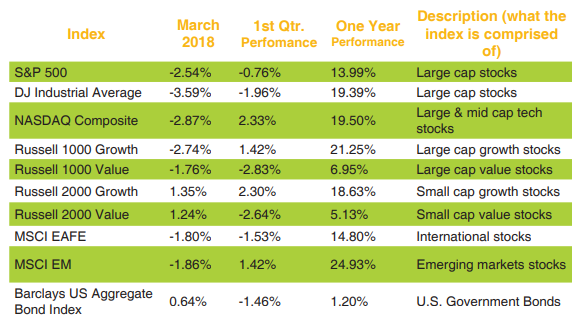

However, on February 2, the January jobs report showed that hourly wages had risen by the most in 8 years, sparking inflation fears and worries that the Fed would raise interest rates faster than they had planned to try to combat inflation. This came at a time when the bond market was already slumping (reportedly because of inflation fears). The yield on the 10-year Treasury note hit a four-year high of 2.85% that same day after starting the year at about 2.4%. Since prices and yields move in opposite directions, this was not a good development and all of this combined to spook stocks, sending the Dow Jones Industrials Average (DJIA) down 666 points or 2.5%, which was the largest percentage decline since Brexit in June of 2016. At that point, the market was just getting warmed up since the next week saw two days where the DJIA declined by 1,000 points or more. By February 8, stocks had entered 10% correction territory, just 2 weeks after making record highs. For a closer look at how various stock and bond asset classes performed in recent periods, please refer to the table.

*as of March 31, 2018

Following the wild week of February 5, stocks did recover about half of the losses experienced during the sharp, brief correction. While President Trump’s rhetoric and actions may have given stocks a boost last year, recent events may be having the opposite effect. Trump made a lot of noise during the election about unfair trade practices of China and others, and announced on March 8 that the US would implement a 25% tariff on steel and 10% on aluminum. At the same time, he said Mexico and Canada would be exempt from the tariffs pending the outcome of ongoing trade negotiations, and that the plan allows other countries to apply for relief from the new duties.

Apart from that, Trump has also criticized Amazon for what he has called “monopolistic tendencies” and has hinted that his administration may take action against the tech giant. Among the critiques is that taxpayers are subsidizing Amazon’s package deliveries because the retailer pays a below market rate to the US Postal Service. Indeed, various studies show that the U.S Post Office should be charging Amazon between $1.25 and $1.46 more per package shipped than it does. Amazon has enjoyed other tax benefits as well, including not being required to charge sales tax in all states that have one until April 1, 2017. Whatever one’s opinion about all of this, Trump’s broadsides against the company appear to have had a real impact, as its stock has dropped by 7% since Axios reported last week that the president had privately expressed a desire to “go after” the online retailer.

It is true that nearly all mainstream economists believe tariffs on imported goods mostly serve as a tax on the consumers of the country levying the tariffs. In response to Trump’s trade rhetoric, China has now announced that it will roll out tariffs on an array of American products. The overall effect of the ongoing tariff talk as well as the anti-Amazon rhetoric has been to keep the stock market off balance. Amazon has been one of the stock market leaders in recent years and its performance has an outsized effect on overall stock market performance because of its giant market capitalization. Another market darling, Facebook, is facing problems of its own with a controversy over how it handles personal data and privacy. As of this writing, the stock is down more than 20% from its all-time high. While it is too early to tell, the current slump in the technology sector, the sector most responsible for the recent stock market leg higher, is not an encouraging sign.

This is not to say that the recent market action is more volatile than normal. Perhaps it seems that way since we experienced so little drama in the market for so long. To illustrate, just prior to the correction, stocks set the record for most number of trading days (around 400) without at least a 5% correction. If one looks back at market history, stocks on average have experienced one 10% correction and four to five 5% corrections during a “typical” year, so last year was definitely an outlier with respect to volatility.

So where does the market go from here? Most stock indices finished the quarter in marginally negative territory, but the damage to the market is a good deal worse if you look at the decline from all-time highs. Raymond James’ market strategist Jeff Saut, who is a bull, pointed out last week right before the quarter end that the S&P 500 had already lost 37% of the market cap it had added since election night back in November 2016. Fast forward a few days into the new quarter and already, we have seen a couple of ugly trading sessions that have stocks near correction territory again. Despite this, if the market can hold the February lows, it is likely that stocks can get back on track.

The last time the market went a record number of trading days without a correction was in the mid-1990’s. Then, the S&P 500 went on to gain for another four years and more than doubled after that streak ended. Times are different now, and the economy and markets seem to be in a more advanced stage of the business cycle. In addition, there is the valuation issue, and valuations of US stocks are rich by any historical measure, possibly even the richest in history when looking at the market as a whole rather than at one sector like technology. We have explained numerous times in these missives that high valuations are not a market-timing indicator and that the psychology of investors must change from risk seeking to risk avoiding for the market to weaken. This is often something that happens slowly, and is why the widely followed declines in market leaders such as Amazon and Facebook should not be ignored.

We are still recommending overweighting foreign stocks. Stocks outside the US lagged for much of the recovery since the financial crisis, so the valuations are significantly lower overall than domestic stocks. Bonds continue to struggle as interest rates creep up and the core bond benchmark has declined 1.64% on an YTD basis as of this writing. With the economy strengthening and the Fed set to normalize rates, we believe that rates will continue to creep up. For bond heavy investors, it may make sense to shorten the duration of your portfolio by introducing PIMCO Short Term into the mix. This would decrease your interest rate risk exposure. You may also consider adding PIMCO Income as a way to gain more exposure to different types of bond investments. Both of these funds can be found in most of our clients’ plans. Whichever category you fall into, now is always a good time to assess your overall retirement portfolio and strategy, so act now to help secure your retirement.

If you have a general administrative question about your account, please contact our customer service at 800-535- 4253 option 1. If you need investment advice, please contact your firm’s designated consultant or me. You can reach me at extension 1178 (510-740-4178) or at john.w@wespac.net. John Williams, Manager of Advisory Services – WESPAC